Payday loans are often seen as a quick fix for unexpected expenses. How Do Payday Loans Work in California, Maybe your car broke down, or you need to cover rent before your next paycheck arrives. In California, payday loans are legal but heavily regulated to protect borrowers from falling into endless debt cycles. Understanding exactly how they work can help you decide whether this type of loan is right for you—or if you should look for safer alternatives.

What Is a Payday Loan?

A payday loan is a small, short-term loan that’s typically due on your next payday. In California, the maximum amount you can borrow from a payday lender is $300, and you must pay it back within 31 days. These loans are designed to cover small, urgent expenses rather than long-term financial needs.

While they seem convenient, payday loans can be expensive. The fees may look small at first, but when calculated as an annual percentage rate (APR), the cost is extremely high—often more than 400% APR.

How Payday Loans Work in California

Here’s how the process usually goes:

-

You apply for the loan.

You can do this at a physical payday lending store or online. You’ll need to show identification, proof of income, and a checking account. -

You write a postdated check or give authorization.

The lender requires either a postdated check for the amount borrowed plus the fee or authorization to electronically withdraw the payment from your bank account on your next payday. -

You receive the money.

Once approved, you’ll get your cash (or direct deposit) almost instantly. -

You repay on your next payday.

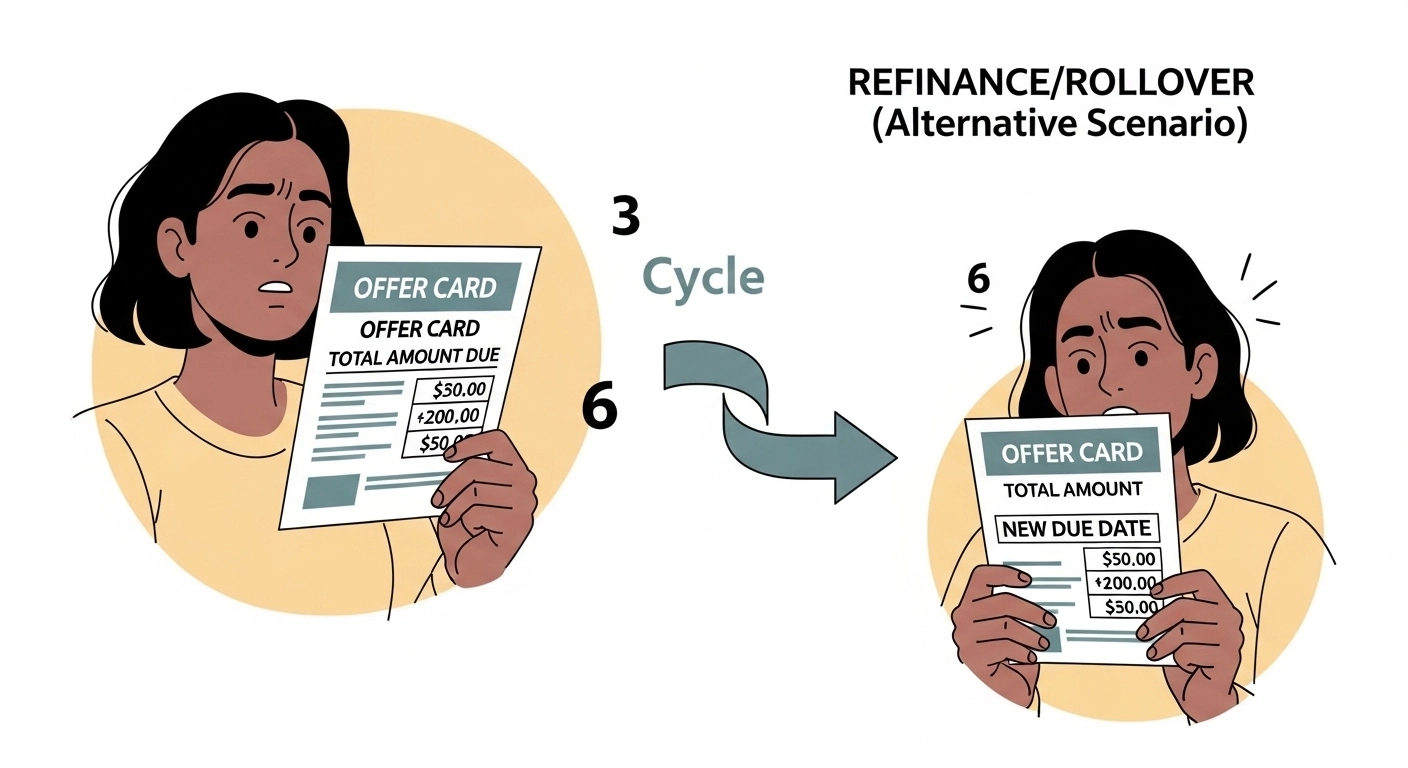

When your payday comes, the lender cashes your check or withdraws the agreed amount. If you can’t pay it off, some lenders might let you “roll over” the loan for another period—but that means paying more fees.

Example of a Payday Loan in California

Let’s say you borrow $300, the legal maximum. California law allows lenders to charge up to $45 in fees for this amount. That means when your payday arrives, you’ll owe $345 total. If you can’t pay it back and decide to roll it over, you’ll owe another $45 in fees the next time—creating a snowball effect that’s hard to escape.

California Payday Loan Regulations

California’s Department of Financial Protection and Innovation (DFPI) oversees payday lending in the state. Here are some key legal protections:

-

Maximum loan amount: $300

-

Maximum fee: $45 (15% of the check amount)

-

Loan term: Up to 31 days

-

No rollovers allowed: Lenders cannot extend or renew a payday loan.

-

Multiple loans: You can’t have more than one payday loan at a time from the same lender.

These rules are designed to prevent predatory lending practices and protect Californians from excessive debt.

The Risks of Payday Loans

Even though payday loans are legal and regulated in California, they still carry significant risks. Some of the most common issues include:

-

Debt cycles: Many borrowers struggle to pay the full amount back, leading to repeated borrowing.

-

High costs: The effective interest rates are extremely high compared to traditional loans or credit cards.

-

Bank account issues: If the lender withdraws money and your balance is low, you could face overdraft fees.

-

Credit impact: While payday loans don’t usually affect your credit score directly, unpaid loans can be sent to collections.

Safer Alternatives to Payday Loans

Before turning to a payday lender, consider other options that might cost less:

-

Ask your employer for an advance. Some companies allow small paycheck advances with no fees.

-

Negotiate with your creditors. Utility companies or landlords may offer short-term extensions.

-

Use a credit union. Many California credit unions offer small personal loans at much lower rates.

-

Explore community programs. Nonprofits and local government offices sometimes provide emergency financial assistance.

Even if you have poor credit, there are increasingly more ethical online lenders that provide installment loans with transparent terms.

Tips for Borrowing Responsibly

If you decide to get a payday loan, take these precautions:

-

Borrow only what you truly need, and ensure you can repay it on time.

-

Compare lenders and confirm they’re licensed in California through the DFPI website.

-

Avoid multiple loans at once—it’s one of the quickest paths to financial stress.

-

Keep a written record of all fees, repayment dates, and contact details.

Final Thoughts

Payday loans in California can help in emergencies, but they should be used with caution. The state’s laws limit how much you can borrow and how much lenders can charge, but the cost is still high compared to other forms of credit. Understanding how payday loans work—and knowing your alternatives—can help you make smarter financial decisions when money is tight.

Empowering you to master your money with confidence and clarity. On this channel, we break down personal finance—from budgeting basics and saving smarter to debt-free strategies and practical investing—all in easy-to-understand language.

Expect weekly deep dives into real-life financial questions, step-by-step tutorials, and expert insights that make money topics approachable and actionable. Whether you’re building emergency savings, paying off loans, or planning for the future, you’re in the right place to get informed, empowered, and financially confident.