Why is your loan rate changing? It’s not about your credit score. Explore how global market indices like SOFR dictate adjustable-rate fluctuations and learn when you should refinance

While personal financial health is always a consideration for lenders, it’s not the primary driver of rate adjustments on an ARM. Instead, external economic forces and the broader financial landscape play a much more dominant role.

This article delves into the key elements that influence your ARM’s interest rate, offering clarity on the forces at play and what borrowers should be aware of. Understanding these dynamics can empower you to make more informed decisions about your mortgage.

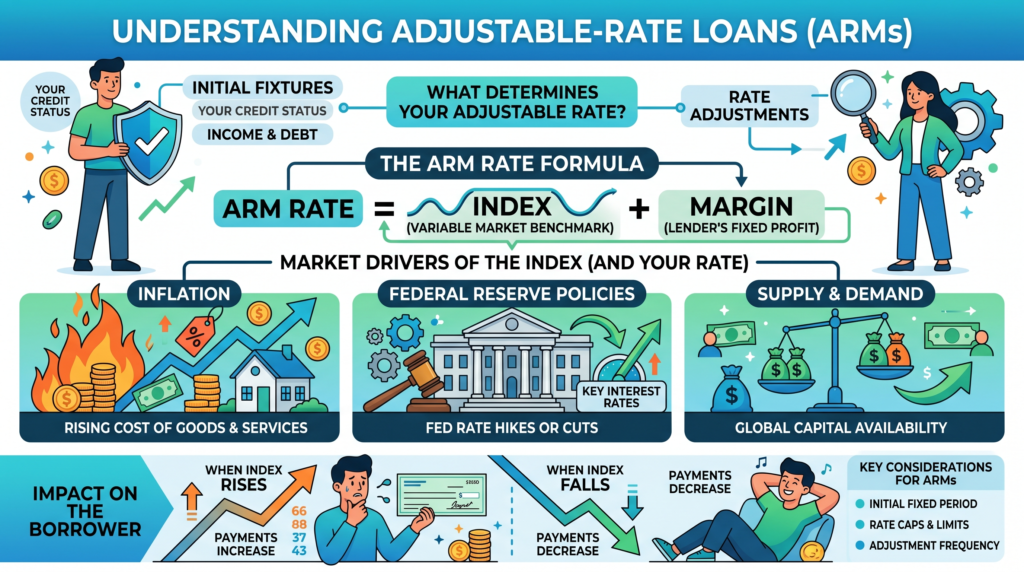

What Best Determines Whether a Borrower’s Interest Rate on an Adjustable Rate Loan Goes Up or Down? The most influential factor is **a market’s condition**. This encompasses a variety of economic indicators that lenders monitor closely when setting and adjusting rates for adjustable-rate mortgages (ARMs).

The Influence of Market Conditions on ARM Rates

When we talk about a market’s condition, we are referring to the overall health and performance of the economy. This includes factors like inflation rates, employment figures, and the general economic growth trajectory. When the economy is expanding and inflation is rising, it often leads to an increase in interest rates across the board, including those for ARMs.

Conversely, during economic downturns or periods of low inflation, interest rates may decrease. Lenders adjust ARM rates based on these broader economic trends, aiming to align their lending practices with the prevailing financial climate. This is a fundamental aspect of how variable interest rate loans function.

Why Bank Finances Aren’t the Primary Driver

While a bank’s financial health is important for its operational stability, it’s not the direct determinant of your individual ARM rate. Banks operate within a larger economic system, and their own financial strategies are often influenced by the same market conditions that affect ARM rates. Therefore, a bank’s internal finances are more of a consequence of market conditions rather than a primary cause of ARM rate changes.

The Limited Impact of a Fixed Interest Rate

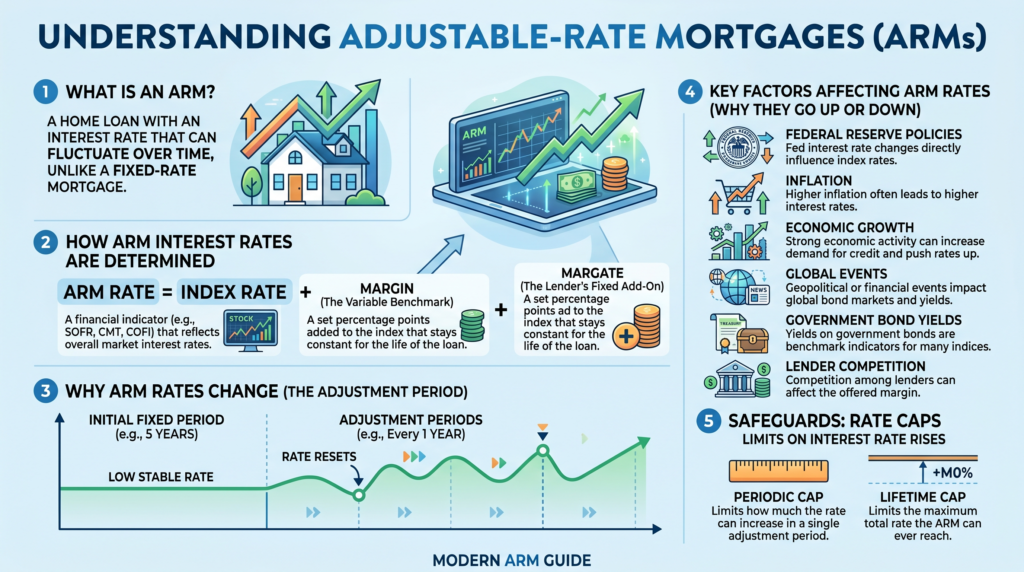

Adjustable-rate mortgages, by their very nature, do not have a fixed interest rate. The defining characteristic of an ARM is that its interest rate can change over the life of the loan. A fixed interest rate is associated with fixed-rate mortgages, which offer stability and predictability, but are a different product altogether.

Personal Finances and ARM Rates

Your personal finances, such as your credit score, income, and debt-to-income ratio, are crucial when you initially qualify for a mortgage. They help determine the initial interest rate you are offered. However, once the loan is originated, these personal financial details do not directly dictate the fluctuations of your ARM’s interest rate. The adjustments are driven by external market forces, as explained by information regarding adjustable rate mortgage interest rate changes.

Understanding these distinctions is key to managing your ARM effectively. By recognizing that market conditions are the primary driver for rate changes, borrowers can better anticipate potential shifts and plan their finances accordingly, as outlined in explanations of why adjustable mortgage rates go up.

FAQ: Understanding Interest Rate Fluctuations in Adjustable-Rate Loans

Navigating the complexities of financing can be challenging. If you’ve noticed your loan payments changing, it’s likely due to broader economic shifts. Here is everything you need to know about why rates fluctuate.

What is the primary factor that determines if an adjustable-rate loan goes up or down?

The market’s condition is the leading driver of interest rate changes for adjustable-rate loans. These loans are specifically designed to respond to the external financial environment rather than the borrower’s personal financial situation.

How do market conditions affect my loan?

When you sign an adjustable-rate contract, the interest rate is tied to external financial indices. These indices act as benchmarks and shift based on major macroeconomic trends, including:

- Federal Reserve Policies: Changes in the federal funds rate set by the central bank.

- Inflation Rates: Rising inflation often leads to higher interest benchmarks.

- Supply and Demand: The global availability of capital and investor behavior.

Which financial indices are commonly used?

Lenders track specific global and national indices to adjust rates. The most prominent examples include:

- SOFR (Secured Overnight Financing Rate): The modern standard for US dollar-denominated loans.

- LIBOR: Historically used, though largely phased out in favor of more transparent indices.

Why doesn’t my personal financial status change the rate?

A common misconception is that a bank’s internal costs or a borrower’s credit score changes the rate mid-loan. While your creditworthiness determines your initial approval and “spread,” the ongoing fluctuations are strictly caused by the market.

Note: A fixed-rate loan, by definition, does not change regardless of market shifts, which is the primary difference from an adjustable-rate loan.

Why is “Market Condition” the correct answer for rate changes?

Macroeconomic trends drive the indices that your loan is pegged to. Neither a bank’s private finances nor a person’s individual financial status has the direct power to move the global indices that dictate interest rate adjustments. Therefore, the condition of the market remains the sole primary factor.

Solution: Managing Your Adjustable-Rate Mortgage (ARM)

The best solution for a borrower facing rising rates is active monitoring and proactive refinancing. Since the market condition is the sole driver of rate changes, you cannot control the rate, but you can control your exposure to it.

- Refinance to a Fixed-Rate Mortgage: If indices like SOFR are trending upward due to inflation, locking in a fixed rate can provide long-term payment stability.

- Rate Caps Awareness: Check your contract for “periodic adjustment caps” which limit how much the interest can rise in a single period.

- Financial Buffering: During low-rate cycles, divert the savings into a high-yield account to offset future market-driven increases.

Summary: Why Rates Change

Interest rates on adjustable loans are not personal; they are professional. They are tied to macroeconomic indices (like SOFR or LIBOR) that fluctuate based on Federal Reserve policies, inflation, and global supply/demand. While your credit score gets you the loan, the market’s condition dictates what you pay month-to-month. Personal finances or bank overhead do not influence these global benchmarks.

Pro Tip for Borrowers

Watch the Fed, not your bank. Because adjustable-rate loans are pegged to market indices, the Federal Reserve’s meetings on inflation are the best “early warning system” for your next payment adjustment. If the Fed signals a hike, it’s time to call a mortgage broker.

Empowering you to master your money with confidence and clarity. On this channel, we break down personal finance—from budgeting basics and saving smarter to debt-free strategies and practical investing—all in easy-to-understand language.

Expect weekly deep dives into real-life financial questions, step-by-step tutorials, and expert insights that make money topics approachable and actionable. Whether you’re building emergency savings, paying off loans, or planning for the future, you’re in the right place to get informed, empowered, and financially confident.